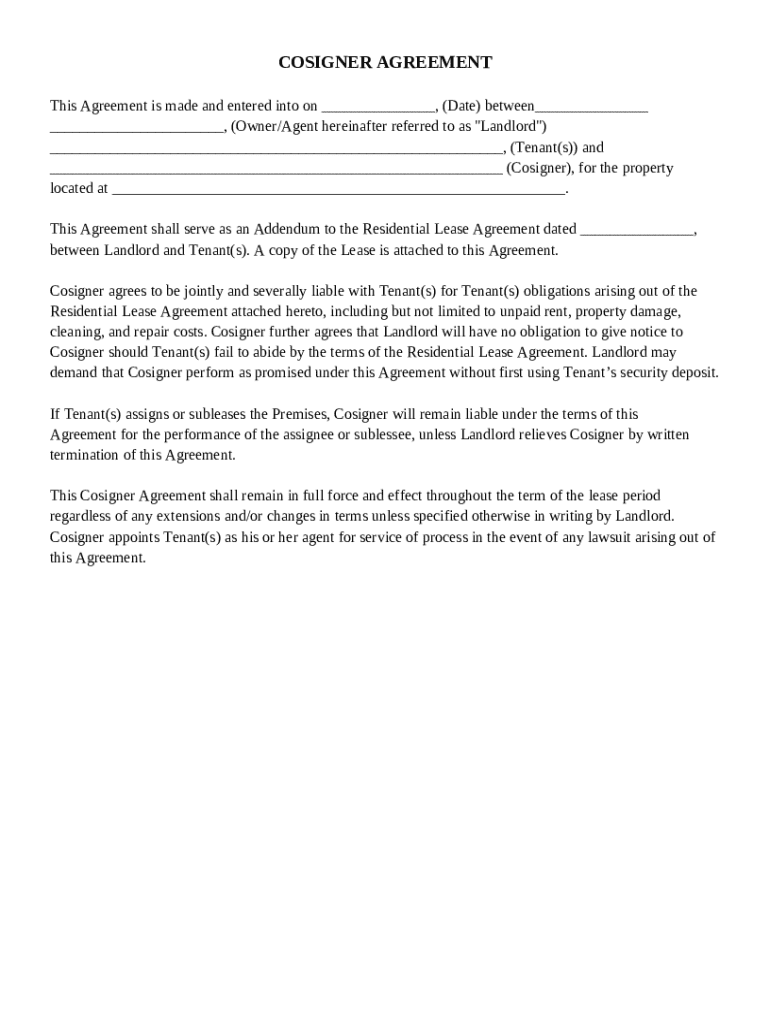

Creating a loan without a cosigner can be a significant hurdle for many individuals seeking financing. While it’s often a requirement, it can also be a barrier to entry for those who lack the financial resources or credit history to secure a traditional loan. This is where a cosigner loan agreement template comes into play. A cosigner loan agreement provides a second source of support, mitigating risk for the lender and offering potential benefits to the borrower. This article will delve into the essential components of a cosigner loan agreement, explaining its purpose, benefits, and crucial considerations. Understanding these aspects is vital for anyone considering a cosigner loan.

What is a Cosigner Loan Agreement?

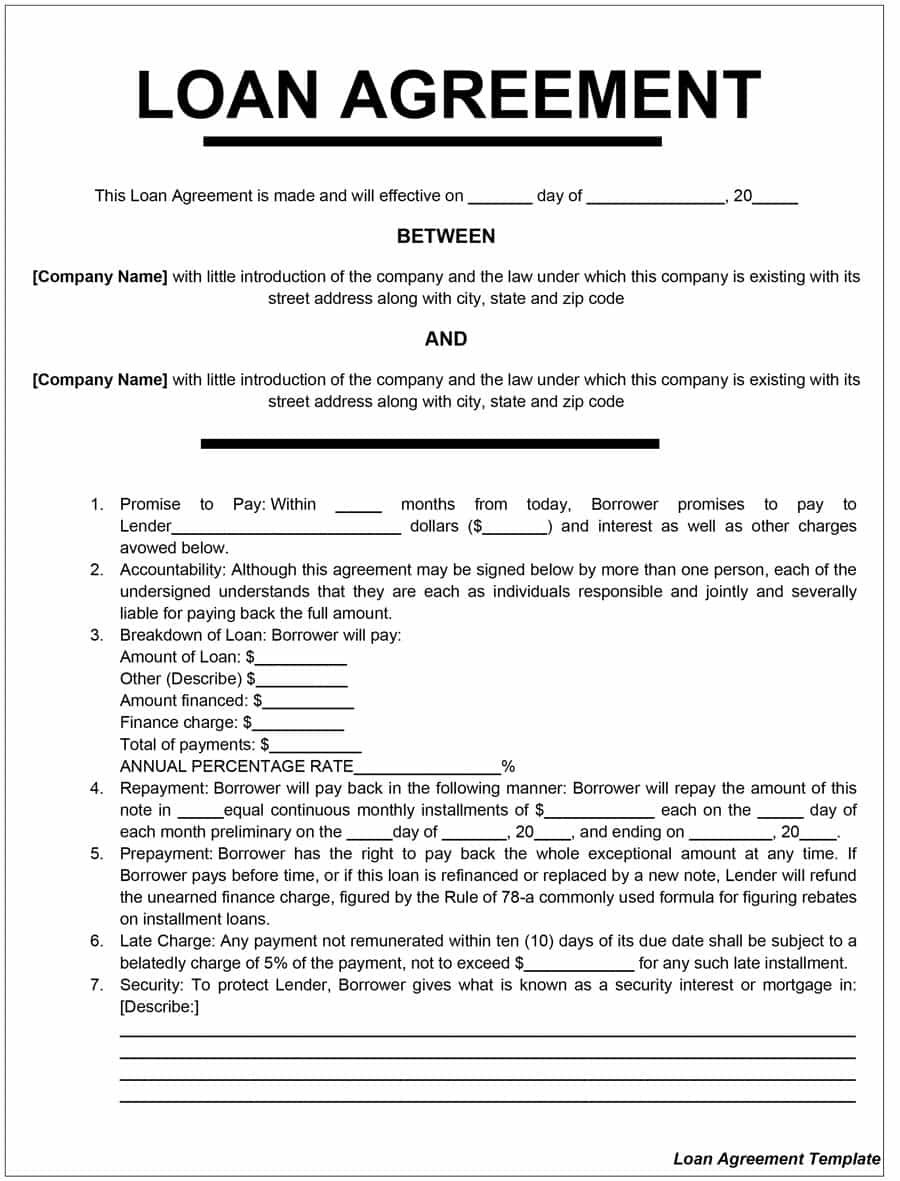

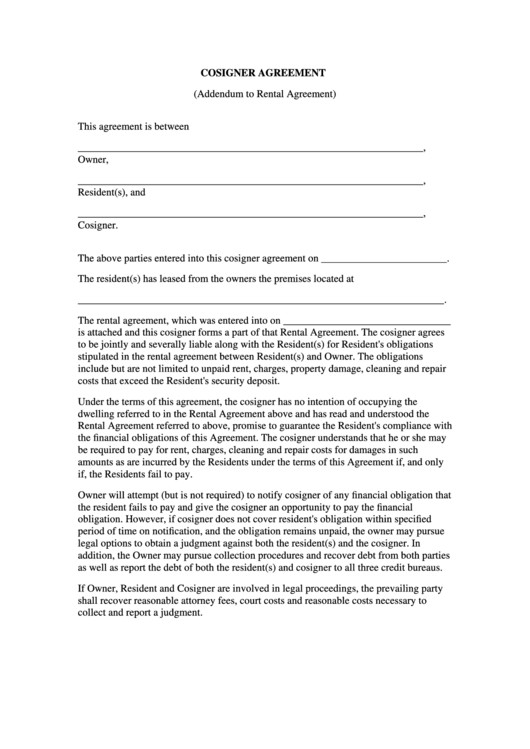

A cosigner loan agreement is a type of loan where one person (the cosigner) agrees to be responsible for repaying the loan if the borrower defaults. It’s a collaborative arrangement where the cosigner’s creditworthiness is leveraged to increase the chances of loan approval. The cosigner’s role is to guarantee the loan, essentially acting as a guarantor. It’s important to note that a cosigner’s credit history and income are scrutinized to assess their ability to repay the loan. The agreement outlines the terms, responsibilities, and potential consequences of the loan. It’s a legally binding document, so it’s crucial to consult with an attorney to ensure it’s properly drafted and protects your interests.

Key Components of a Cosigner Loan Agreement

A comprehensive cosigner loan agreement typically includes the following key elements:

- Loan Amount and Purpose: Clearly define the amount of the loan and the specific purpose for which it’s being used. This provides context for the lender and helps ensure the loan is appropriate.

- Cosigner Information: Specify the full legal name, address, and contact information of the cosigner. Include their relationship to the borrower.

- Agreement to Cosign: The cosigner’s explicit agreement to be liable for the loan if the borrower defaults. This is a fundamental requirement.

- Repayment Terms: Outline the proposed repayment schedule, including the frequency of payments, the interest rate (if any), and the total repayment amount.

- Default Provisions: Define what constitutes a default, including late payments, missed payments, or failure to provide required documentation.

- Collateral (if applicable): If the loan is secured by collateral (e.g., a vehicle or property), specify the collateral and its value.

- Legal Fees: Address the costs associated with drafting and reviewing the agreement.

- Governing Law: Specify the state or jurisdiction whose laws will govern the agreement.

Benefits of Using a Cosigner

For borrowers, a cosigner loan can be a significant advantage. Here’s why:

- Increased Approval Odds: A cosigner’s credit history and income can significantly improve the borrower’s chances of loan approval, especially for those with limited credit scores or a lack of collateral.

- Lower Interest Rates: Lenders may be more willing to offer lower interest rates to cosigners, as they are considered a lower risk.

- Easier Access to Financing: A cosigner can make it easier to qualify for a loan, particularly for individuals who may not meet the standard requirements for a traditional loan.

- Financial Support: The cosigner’s repayment helps the borrower maintain their financial stability and reduces the risk of default.

Understanding the Role of the Cosigner

The cosigner’s responsibilities are crucial. They are legally obligated to repay the loan if the borrower fails to do so. This means:

- Financial Responsibility: The cosigner must be able to comfortably afford the loan payments.

- Disclosure: The cosigner must fully disclose their financial situation to the lender.

- Cooperation: The cosigner must cooperate with the lender and provide any necessary documentation.

- Legal Consequences: Failure to uphold their commitment can result in legal action, including the cosigner’s liability for the loan.

Types of Cosigner Loans

There are various types of cosigner loans, each with slightly different terms and conditions:

- Traditional Cosigner Loan: This is the most common type, where the cosigner agrees to be responsible for the loan.

- Co-signed Credit Card: A co-signed credit card allows the cosigner to have a credit line, but the cosigner is ultimately responsible for the debt.

- Co-signed Auto Loan: Similar to a credit card, but for a vehicle.

- Co-signed Personal Loan: A personal loan where the cosigner is responsible for the loan.

Important Considerations Before Signing

Before entering into a cosigner loan agreement, it’s essential to carefully consider the following:

- Credit Score: Assess your own credit score and determine if you can qualify for a cosigner loan.

- Financial Stability: Ensure you can comfortably afford the loan payments without jeopardizing your own financial stability.

- Relationship with the Cosigner: Consider the potential impact on your relationship with the cosigner.

- Terms and Conditions: Thoroughly review all the terms and conditions of the agreement to understand your obligations and responsibilities.

- Legal Advice: Consult with an attorney to ensure the agreement is legally sound and protects your interests.

Conclusion

A cosigner loan agreement can be a valuable tool for individuals seeking financing, particularly those who lack the required credit history or collateral. However, it’s crucial to understand the responsibilities and potential risks involved. By carefully considering the key components of a cosigner loan agreement and seeking professional legal advice, borrowers can make informed decisions and secure a loan that aligns with their financial goals. Remember, a well-structured agreement protects both the borrower and the lender, fostering a collaborative and mutually beneficial relationship. The core principle remains: a cosigner’s commitment to repaying the loan is paramount to the success of the agreement.